Life insurance with pancreatitis is not too difficult for most.

If you’ve had or have pancreatitis, and life insurance is a necessity for you, you’re in the right place. This post discusses what factors are the major concerns when applying for life insurance with pancreatitis.

You may have been wrongfully declined, but don’t lose hope. It’s quite possible there’s a chance you just didn’t find the right company to work with, and we can help you get paired correctly.

Depending on what type you have, life insurance with pancreatitis can be awarded as high as select preferred! The best rating in the industry!

If you’re looking for more information about buying life insurance with pancreatitis, keep reading.

Finding Life Insurance With Pancreatitis

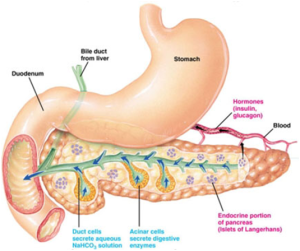

Pancreatitis comes about in many ways, and the symptoms vary for each person. There are also different types, so classifying what type of pancreatitis you suffered from or currently suffer from make a difference. Life insurance underwriters are primarily focused on the long term effect of your pancreatitis, so you just need to make a solid case for yourself when you apply, and that’s where we come in.

When anyone is looking for life insurance with pancreatitis, we walk them through the same questionnaire each time. Here’s what we need to know:

- Type of Pancreatitis

- Dates of Concern

- Symptoms

- Cause

There are two types of pancreatitis: acute and chronic. If your particular case is acute, this is obviously the best case scenario, as long as the instances are limited. You could have an acute case of pancreatitis once, or it could return multiple times without still being declared chronic. If this is the case, extra details will be required, and we’ll get to that in a second. If your case is chronic, meaning you’ll be dealing with it for a long period of time, and it could be the root cause for more serious health conditions.

If you suffered only a single case of acute pancreatitis, resulting from something like gallstones, you can probably expect the top tier rates so long as the rest of your health is in order. A single case of pancreatitis is relatively easily treated (even though it can have severe consequences if not treated quickly enough), and there is no long term damage to the pancreas itself. Assuming it recovers fully, your body can continue to function and your long term health is pretty much unaffected.

If you’ve suffered from multiple bouts of acute pancreatitis, the cause becomes a bigger issue. Acute pancreatitis can be caused by alcohol abuse, sustained use of drugs, or viral infections. If alcohol is the cause, you might only be able to apply after you can submit viable documentation you’ve discontinued your use. The wait time varies per company, and you’d be looking at 1 to 2 years before you can apply under normal circumstances.

The time frame in which the acute pancreatitis occurred is relevant, although it’s not extremely important unless you’ve dealt with it multiple times. As long as the pancreatitis has dissipated at least a few weeks ago, you’ll be just fine to apply. However, with multiple cases, another time frame may be suggested based on duration and frequency. The more occurrences or higher frequency, the longer you’ll need to wait. Knowing your dates of diagnosis are key, and the underwriter may want to see them to verify.

While symptoms and treatments (although treatments aren’t direct) aren’t the main focus, they can become a bigger concern if any long term harm has occurred. When the pancreas fails, it can affect blood pressure, the kidneys, the respiratory system and even the heart. If these have been harmed or symptoms linger long after the pancreatitis has subsided, additional underwriting is probable. Your entire health profile is reviewed before any rating is given, so this area could not only extend the time it takes to get approved, but could result in a loss of discounts or even a rated policy, depending on severity.

On the other hand, if your pancreatitis is chronic, it is no longer the main issue. The cause is now the larger concern. Chronic pancreatitis can be hereditary or resulting from other diseases such as hemochromatosis. The damage to the pancreas is irreversible, and this results in other organ or system failure over time. Your entire health profile is critical at this point, so applying sooner than later is your best bet. With chronic pancreatitis, you can expect a rated policy most of the time, with a very small chance of a standard rating if your health is otherwise still good.

If you or someone you know has any concern about getting life insurance with pancreatitis, please contact us today. We can give you accurate quotes so you can have a more realistic expectation before purchasing. Our goal is find you the right carrier, and get you covered at the most affordable rates, and we won’t stop working until we feel we’ve accomplished this.

Speak Your Mind